"Can I use Pix?"

Understanding the relationship between investor and the banking services in the financial market.

Date

July 2021 - October 2021

Roles

Research and dynamics

Study of limitations and regulations

Benchmark

Interface creation

Usability tests

Metrics for continuous improvement

Challenge

Understand customer receptivity to a new card, identifying trends and creating a relevant solution.

Scenario

In the second quarter of 2021, Órama Investimentos' Banking squad received a new prioritization: the creation of a credit card. The deadline for delivery was short, and there were still many uncertainties.

Research results

932 participants

Base: Customers who had already made at least 1 deposit

Do you use a credit card monthly?

56,1% YES, one card.

35,5% YES, +1.

YES 91,6%

What would make you request a new card?

1. Annual fee exemption.

(58.2% / 527 part)

2. Cashback.

(46,5% / 421 part)

3. Fidelity program.

(33,8% / 306 part)

From the financial services below, which one(s) do you use at least once a month?

(participant could choose up to 3 options)

1. Credit card.

(79,7% / 743 part)

2. Transfers to banks.

(76,6% / 714 part)

3. Bill payment.

(76,5% / 713 part)

4. Pix.

(71,7% / 668 resp)

5. Debit card.

(56,4% / 526 part)

From the options below, which one(s) would you like to have at Órama?

(participant could choose up to 3 options)

1. Value transfer via Pix. (50,6% / 472 part)

2. Automatically reinvested cashback. (35,5% / 334 part)

3. Cashback so I can withdraw the money. (23,3% / 217 part)

4. Credit Card. (22,4% / 209 part)

5. Transfer to other titularyties. (21,1% / 197 part)

Insights

Although our customers are interested in a company credit card (22.4%), only 35.5% of them use more than one card monthly. As it is a competitive market, it creates a scenario in which we would need to offer many differentiators in order to attract a small portion that had shown interest.

Pix (instant payment system) was not only the most requested with 50.6%, but it would also solve other pain points that exist today, such as transfers between different titularyties that currently do not exist and the delay of up to 2 hours to confirm a deposit of the TED transaction model (until then the only way to bring resources in).

We had identified and defined a new problem:

The brokerage's transfer of values is still archaic and traditional. Customers want to control their Órama balance in a simpler, more practical and faster way.

Benchmark

Understanding the different types of participation in Pix, we tried to launch an MVP that would only allow us to bring financial resources (a model widely used by e-commerce for payments). This would help mainly in the company's campaigns, as it would allow users to have this resource instantly to invest in the advertised products.

Sprint Zero

Even knowing that the credit card represented a strategic objective for the company, it was evident that many steps were ignored, they had practically skipped the first diamond of understanding the problem (discovery and analysis).

We then looked for an approach that would prepare us technically to create what was requested, but that would also allow some validation as to whether that was really the best path to follow.

We needed to understand our user's pains and problems before defining the final solution.

General objectives:

Discover the pains and desires of our customers.

Understand different financial profiles.

Understand customer relationships with digital solutions in the financial market.

Map out interesting financial products for them.

Key questions:

Is there a demand for another credit card?

What new feature/product do our users miss the most?

Research objectives

In the first few days, we met with the entire squad to start a CSD matrix, raising the certainties, assumptions and doubts that surrounded the project. In these meetings it became clear that there were still many uncertainties among all team members, therefore identifying the general objectives and key questions for qualitative research.

Handoff

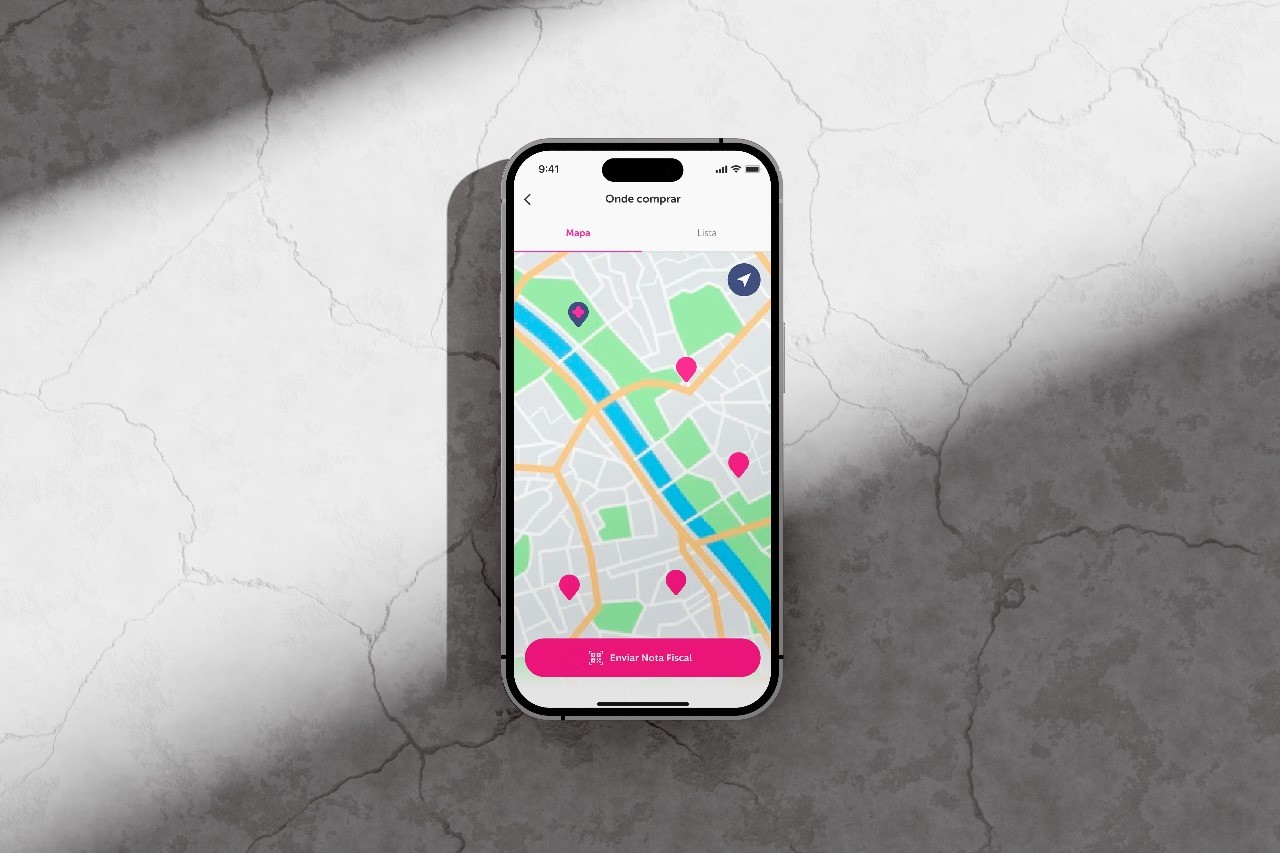

When we defined the path to be followed, we broke the flows into stories and prioritized which ones should reach the developers' hands first. Below are the interfaces delivered between 4 sprints.

Access and Home Pix

Onboarding

Receiving Pix

Pix Transfer

Pix QR Code Payment

Receipt and Balance

Filling fields

Error scenarios

Next project

Contact

"Can I pay with Pix?"

Understanding the relationship between investor and the banking services in the financial market.

Date

July 2021 - October 2021

Roles

Metrics for continuous improvement

Usability tests

Interface creation

Benchmark

Study of limitations and regulations

Research and dynamics

Scenario

In the second quarter of 2021, Órama Investimentos' Banking squad received a new prioritization: the creation of a credit card. The deadline for delivery was short, and there were still many uncertainties.

Challenge

Understand customer receptivity to a new card, identifying trends and creating a relevant solution.

Sprint Zero

Even knowing that the credit card represented a strategic objective for the company, it was evident that many steps were ignored, they had practically skipped the first diamond of understanding the problem (discovery and analysis).

We then looked for an approach that would prepare us technically to create what was requested, but that would also allow some validation as to whether that was really the best path to follow.

We needed to understand our user's pains and problems before defining the final solution.

General objectives:

Discover the pains and desires of our customers.

Understand different financial profiles.

Understand customer relationships with digital solutions in the financial market.

Map out interesting financial products for them.

Key questions:

Is there a demand for another credit card?

What new feature/product do our users miss the most?

Research objectives

In the first few days, we met with the entire squad to start a CSD matrix, raising the certainties, assumptions and doubts that surrounded the project. In these meetings it became clear that there were still many uncertainties among all team members, therefore identifying the general objectives and key questions for qualitative research.

Research results

932 participants

Base: Customers who had already made at least 1 deposit

Do you use a credit card monthly?

56,1% YES, only one card.

35,5% YES, more than one card.

YES 91,6%

{

What would make you request a new card?

1. Annual fee exemption. (58.2% / 527 part)

2. Cashback. (46,5% / 421 part)

3. Fidelity program. (33,8% / 306 part)

From the financial services below, which one(s) do you use at least once a month?

(participant could choose up to 3 options)

1. Credit card. (79,7% / 743 part)

2. Transfers to banks. (76,6% / 714 part)

3. Bill payment. (76,5% / 713 part)

4. Pix. (71,7% / 668 resp)

5. Debit card. (56,4% / 526 part)

From the options below, which one(s) would you like to have at Órama?

(participant could choose up to 3 options)

1. Value transfer via Pix. (50,6% / 472 part)

2. Automatically reinvested cashback. (35,5% / 334 part)

3. Cashback so I can withdraw the money. (23,3% / 217 part)

4. Credit Card. (22,4% / 209 part)

5. Transfer to other titularyties. (21,1% / 197 part)

Insights

Although our customers are interested in a company credit card (22.4%), only 35.5% of them use more than one card monthly. As it is a competitive market, it creates a scenario in which we would need to offer many differentiators in order to attract a small portion that had shown interest.

Pix (instant payment system) was not only the most requested with 50.6%, but it would also solve other pain points that exist today, such as transfers between different titularyties that currently do not exist and the delay of up to 2 hours to confirm a deposit of the TED transaction model (until then the only way to bring resources in).

We had identified and defined a new problem:

The brokerage's transfer of values is still archaic and traditional. Customers want to control their Órama balance in a simpler, more practical and faster way.

Benchmark

Understanding the different types of participation in Pix, we tried to launch an MVP that would only allow us to bring financial resources (a model widely used by e-commerce for payments). This would help mainly in the company's campaigns, as it would allow users to have this resource instantly to invest in the advertised products.

Handoff

When we defined the path to be followed, we broke the flows into stories and prioritized which ones should reach the developers' hands first. Below are the interfaces delivered between 4 sprints.

Access and Home Pix

Onboarding

Receiving Pix

Pix Transfer

Pix QR Code Payment

Receipt and Balance

Filling fields

Error scenarios

Understanding the relationship between investor and the banking services in the financial market.

"Can I pay with Pix?"

Date

July 2021 - October 2021

Scenario

Challenge

Roles

Research and dynamics

Study of limitations and regulations

Benchmark

Interface creation

Usability tests

Metrics for continuous improvement

In the second quarter of 2021, Órama Investimentos' Banking squad received a new prioritization: the creation of a credit card. The deadline for delivery was short, and there were still many uncertainties.

Understand customer receptivity to a new card, identifying trends and creating a relevant solution.

Sprint Zero

Even knowing that the credit card represented a strategic objective for the company, it was evident that many steps were ignored, they had practically skipped the first diamond of understanding the problem (discovery and analysis).

We then looked for an approach that would prepare us technically to create what was requested, but that would also allow some validation as to whether that was really the best path to follow.

We needed to understand our users' pains and problems before defining the final solution.

General objectives:

Discover the pains and desires of our customers.

Understand different financial profiles.

Understand customer relationships with digital solutions in the financial market.

Map out interesting financial products for them.

Key questions:

Is there a demand for another credit card?

What new feature/product do our users miss the most?

Research objectives

In the first few days, we met with the entire squad to start a CSD matrix, raising the certainties, assumptions and doubts that surrounded the project. In these meetings it became clear that there were still many uncertainties among all team members, therefore identifying the general objectives and key questions for qualitative research.

Do you use a credit card monthly?

56,1% YES, only one card.

35,5% YES, more than one card.

YES 91,6%

{

What would make you request a new card?

1. Annual fee exemption. (58.2% / 527 part)

2. Cashback. (46,5% / 421 part)

3. Fidelity program. (33,8% / 306 part)

From the financial services below, which one(s) do you use at least once a month?

(participant could choose up to 3 options)

1. Credit card. (79,7% / 743 part)

2. Transfers to banks. (76,6% / 714 part)

3. Bill payment. (76,5% / 713 part)

4. Pix. (71,7% / 668 part)

5. Debit card. (56,4% / 526 part)

From the options below, which one(s) would you like to have at Órama?

(participant could choose up to 3 options)

1. Value transfer via Pix. (50,6% / 472 part)

2. Automatically reinvested cashback. (35,5% / 334 part)

3. Cashback so I can withdraw the money. (23,3% / 217 part)

4. Credit Card. (22,4% / 209 part)

5. Transfer to other titularyties. (21,1% / 197 part)

Research results

932 participants

Base: Customers who had already made at least 1 deposit in the company

Insights

Although our customers are interested in a company credit card (22.4%), only 35.5% of them use more than one card monthly. As it is a competitive market, it creates a scenario in which we would need to offer many differentiators in order to attract a small portion that had shown interest.

Pix (instant payment system) was not only the most requested with 50.6%, but it would also solve other pain points that exist today, such as transfers between different titularyties that currently do not exist and the delay of up to 2 hours to confirm a deposit of the TED transaction model (until then the only way to bring resources in).

We had identified and defined a new problem:

The brokerage's transfer of values is still archaic and traditional. Customers want to control their Órama balance in a simpler, more practical and faster way.

Benchmark

Understanding the different types of participation in Pix, we tried to launch an MVP that would only allow us to bring financial resources (a model widely used by e-commerce for payments). This would help mainly in the company's campaigns, as it would allow users to have this resource instantly to invest in the advertised products.

Handoff

When we defined the path to be followed, we broke the flows into stories and prioritized which ones should reach the developers' hands first. Below are the interfaces delivered between 4 sprints.

Access and Home Pix

Onboarding

Receiving Pix

Pix Transfer

Pix QR Code Payment

Receipt and Balance

Filling fields

Error scenarios

Roadmap

After handoff:

Due to the deadline, we were able to test quickly with acquaintances (Friends and Family Test).

First internal-only release for technical validations. This period would be important for collecting feedback and would also give us time to properly test the flows with real users. This dynamic is not ideal as it can generate rework, but it was necessary to not miss the window of opportunity for the solution.

Next steps:

Usability tests with real users and collect feedback from the company’s “beta testers”.

Revisit flows that require adjustments, aligning the impacts of changes with developers.

As Pix is an incipient solution, keep the product updated with constant feature launches, also aiming to ensure that it remains regulatory validated.

Monitor usage metrics to identify points for improvement or new business opportunities.